Tax Saving Strategy: Cost Segregation & Bonus Depreciation

1. Real Estate Depreciation

Depreciation is a “phantom expense.” The IRS assumes that buildings wear out, decay, or

become obsolete over time. Therefore, they allow you to deduct a portion of the building’s

value from your income every year, even if the property is actually increasing in market value.

The Calculation: You cannot depreciate the value of land (because land doesn’t “wear out”).

You only depreciate the improvement (the building).

Residential: Total Building Value ÷ 27.5 years.

Commercial: Total Building Value ÷ 39 years.

Why it’s a “Phantom”: You aren’t actually writing a check for this expense. Your bank

account stays the same, but your taxable income goes down on paper.

Example: If you buy a rental house (excluding land value) for $275,000:

$275,000 ÷ 27.5 years = $10,000 annual depreciation deduction.

Even if you made $10,000 in actual profit, the IRS sees $0 in taxable income because of this deduction.

2. Tax Deductions

A tax deduction (or “write-off”) is any “ordinary and necessary” expense incurred to manage, conserve, or maintain your investment property.

These expenses are subtracted from your Gross Income to arrive at your Taxable Income.

Common real estate deductions include:

Mortgage Interest: Usually the biggest deduction.

Property Taxes: State and local taxes paid on the property.

Operating Expenses: Repairs, maintenance, utilities, insurance, and property management fees.

Travel & Education: Mileage driven to visit the property or costs for real estate seminars.

The “Big One”: Depreciation (as explained above).

3. How They Work Together (The Formula)

The goal of a real estate investor is to have Positive Cash Flow but a Negative Taxable Income.

4. Cost Segregation

Typically, residential real estate is depreciated over 27.5 years, and commercial property over 39 years in equal annual increments.

However, many components within a building wear out much faster than 27.5 years.

The Concept: It is an engineering-based analysis that breaks a building down into its

individual components rather than treating it as one solid structure.

Classification Categories:

5 or 7-Year Property: Flooring/Carpeting, specialty lighting, appliances, and furniture

(Personal Property), Wall coverings, Window treatment, Built-in cabinetry,

15-Year Property: Landscaping, fencing, and paved parking lots, Sidewalk (Land

Improvements), Signage, Sprinklers, Stormwater drainage pipes and catch basins

The Effect: By reclassifying these items into shorter lifespans, you can accelerate your

depreciation deductions significantly in the early years of ownership.

5. Bonus Depreciation

Bonus Depreciation is a tax incentive that allows you to deduct a large percentage of the

cost of eligible assets (those with a lifespan of 20 years or less identified via Cost Segregation) immediately in the first year.

Current Status (2026): Under current tax laws as of early 2026, the 100% Bonus

Depreciation remains a powerful tool for qualifying assets placed in service.

How it Works: If a Cost Segregation study identifies 20% of a $1M building ($200,000) as

5-year or 15-year property, you can potentially deduct the entire $200,000 in Year 1 using

the 100% Bonus Depreciation rule.

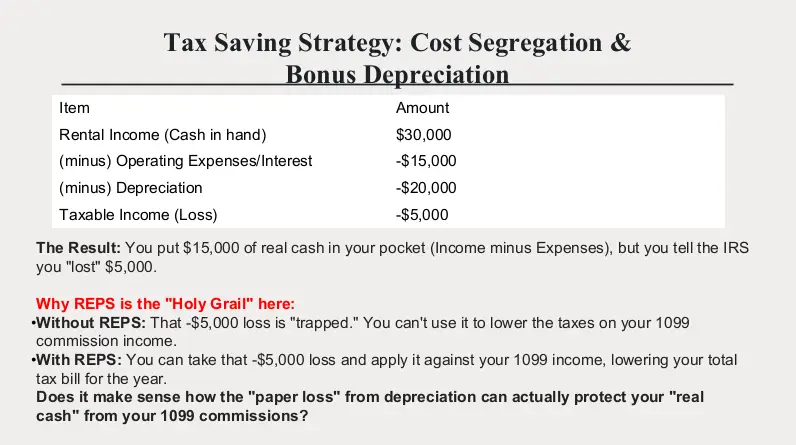

6. Synergy with REPS (Why Combine Them?)

For a standard investor without REPS, these large “paper losses” created by depreciation

are “passive losses,” meaning they can usually only offset rental income.

However, for a 1099 Real Estate Agent with REPS, the magic happens here:

Offset Active Income: You can use the massive depreciation loss from your rentals to

wipe out the taxable income from your 1099 commissions.

Tax Neutrality: If you earned $200,000 in commissions and generated $200,000 in

depreciation via Cost Segregation, your taxable income becomes $0.

Compound Growth: You keep the cash that would have gone to the IRS and use it as a

down payment for your next investment property.

A Note on Depreciation Recapture

Keep in mind that when you eventually sell the property, the IRS may

“recapture” that depreciation and tax it.

This strategy is most effective if you plan to hold long-term or use a 1031 Exchange to defer those taxes indefinitely.

Join The Discussion